This week’s crypto digest highlights a mix of market-moving developments, industry consolidation, and shifting institutional interest. From unexpected cultural crossover in Drake’s new album referencing high-profile crypto figures to continued pressure in Ethereum’s rollup ecosystem following Syndicate Labs’ shutdown, the sector showed both volatility and structural change.

But first, let's see the top gainer and loser cryptos of the week, according to CoinMarketCap data.

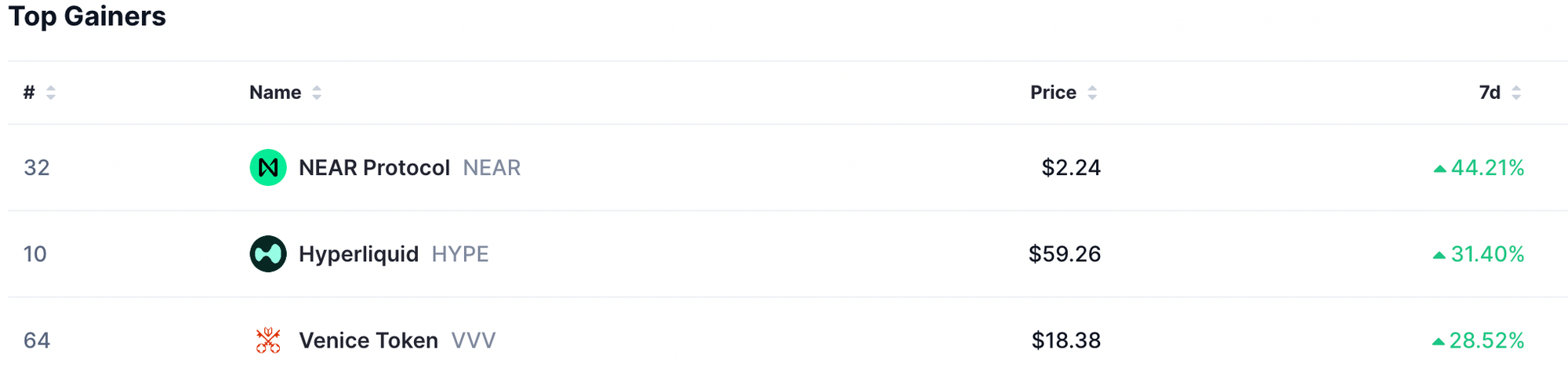

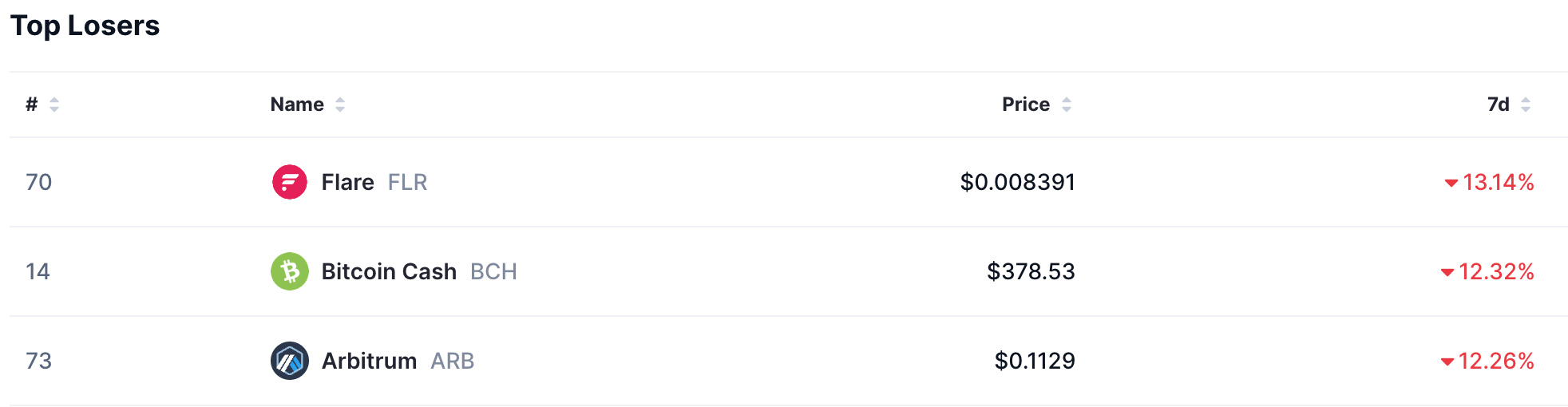

Top gainers and losers of the week

- NEAR Protocol (NEAR) - jumped by 44.21% to $2.24 this week;

- Hyperliquid (HYPE) - surged 31.40% during that time to reach a price of $59.26;

- Venic Token (VV) - The price went up 28.52% to $18.38.

- Flare (FLR) - end week price of $0.008391, falling this week by 13.14%.

- Bitcoin Cash (BCH) - lost 12.32% to end the week at a price of $378.53.

- Arbitrum (ARB) - finished the week down 12.26%, at $0.1129;

Drake references Sam Bankman-Fried pardon in new album release

Drake has returned to music with a surprise triple album release featuring 43 new tracks, including an unexpected reference to imprisoned FTX founder Sam Bankman-Fried. The rapper appears to call for his release on the song “Dust” from the album Iceman, drawing attention from both music and crypto audiences.

In the track, Drake sings:

“An FTX penthouse high-riser, yeah,” followed by, “Samuel Bankman, free all my guys up, yeah.” The lyrics also include a self-description as “a BTC crypto big-timer,” signaling continued engagement with cryptocurrency themes in his music.

The release comes after years of public scrutiny and artistic rivalry that reshaped Drake’s recent career narrative. The new albums, however, have received a mixed to negative critical response. The Guardian described the project as a “boring, bloated disaster,” reflecting early media reaction to the 43-track rollout.

Sam Bankman-Fried, the former CEO of FTX, is currently serving a 25-year federal prison sentence in California after being convicted of fraud related to the collapse of the crypto exchange. Despite his conviction, he and his family have continued to seek a presidential pardon, including renewed efforts following Donald Trump’s return to office.

Trump has publicly stated he has no plans to pardon Bankman-Fried. Meanwhile, the crypto industry has largely distanced itself from the former billionaire, citing reputational concerns.

Drake’s own ties to the crypto sector have also drawn scrutiny. He has faced legal disputes related to his promotion of Stake, a crypto-based online gambling platform, adding further attention to his references to digital assets and high-profile crypto figures.

Syndicate Labs shuts down as Ethereum rollup sector contracts

Syndicate Labs has announced it will wind down operations after five years of building infrastructure for Ethereum rollups and customizable sequencers, citing a sharp contraction in the rollup market and declining demand for its technology.

The venture-backed company confirmed the decision on Thursday via X, stating that “the rollup market has fundamentally shifted.”

Syndicate Labs is winding down.

— Syndicate (@syndicateio) May 21, 2026

After five years building onchain developer infrastructure, the rollup market has fundamentally shifted, making this decision necessary.

Here's what this means for the network, token holders, and developers building with Syndicate.

Syndicate Labs focused on building customizable Ethereum appchains and application-specific rollups using programmable sequencers. The company raised $20 million in Series A funding in 2021, led by Andreessen Horowitz.

The shutdown comes during a period of consolidation in Ethereum’s layer-2 ecosystem. Data from L2Beat shows that Arbitrum One, Base, and OP Mainnet dominate the sector, controlling roughly 75% of total rollup market share. Smaller networks have struggled to maintain liquidity and user activity as capital concentrates around leading platforms.

Syndicate said the market shift reduced demand for its model. It stated that custom chains are increasingly being built by consulting teams from scratch, reducing reliance on reusable infrastructure and shared network tools.

The company also clarified that its Syndicate Network Collective remains independent, and SYND token governance is not directly affected. It said the decision to wind down was unrelated to a recent bridge exploit involving the Syndicate Commons Bridge on Base, which led to a loss of 18.5 million SYND tokens worth about $330,000.

Syndicate Labs joins a growing list of DeFi and crypto projects closing operations this year, including Legend, Step Finance, Polynomial, Balancer Labs, and Seamless Protocol, reflecting broader pressure across decentralized finance infrastructure projects.

Zerohash targets new funding round after Mastercard deal shift

Crypto infrastructure firm Zerohash is seeking a new funding round at a valuation above the $1.5 billion level discussed earlier this year, following changes in Mastercard’s stablecoin investment strategy, according to reporting from CoinDesk.

The discussions come after Mastercard reportedly stepped back from a potential investment in the Chicago-based company and redirected its focus toward another stablecoin infrastructure deal. A Zerohash spokesperson said the company “doesn’t comment on fundraising conversations.”

Mastercard had considered a strategic investment in Zerohash and even explored a potential acquisition valued between $1.5 billion and $2 billion. That deal was described as one of the company’s larger moves into stablecoin infrastructure before priorities shifted.

Mastercard has since moved forward with a different transaction in the sector. In March, the payments giant agreed to acquire BVNK, a stablecoin infrastructure provider, in a deal worth up to $1.8 billion including $300 million in contingent payments. The company said the acquisition aims to connect on-chain payments with traditional fiat rails.

Zerohash continues to position itself as a key player in digital asset infrastructure. The company provides APIs that allow banks, brokerages, and fintech firms to integrate crypto trading, stablecoin payments, and tokenized assets without building blockchain systems internally. Its services include custody, compliance, liquidity, settlement, and blockchain connectivity.

The firm was valued at $1 billion in September 2025 after raising $104 million in a Series D-2 round led by Interactive Brokers.

Zerohash has said its infrastructure has supported more than 5 million users across 190 countries and has powered products for firms including Interactive Brokers, Stripe, Shift4, Franklin Templeton, DraftKings, Kalshi, Lightspark, Tastytrade, and Republic.

The renewed fundraising effort signals continued investor interest in stablecoin infrastructure, even as major payment networks refine their strategies through acquisitions and partnerships across the sector.

South Carolina enacts sweeping crypto rights law

South Carolina has passed new legislation establishing a broad regulatory framework for cryptocurrency use, self-custody, and mining, marking one of the most detailed state-level crypto laws in the United States.

Governor Henry McMaster signed S. 163 into law on Tuesday, updating the South Carolina Code of Laws to formally recognize digital asset activity and limit state-level restrictions on crypto users and businesses.

The law explicitly states that individuals and companies cannot be prevented from accepting cryptocurrency as payment for goods and services. It also protects the use of self-hosted and hardware wallets, allowing residents to fully control their digital asset holdings without third-party custody requirements.

Under the new framework, cryptocurrencies used for payments are exempt from additional state or local taxation, withholding, or special charges.

A key component of the legislation is its stance on central bank digital currencies. The law prohibits any state agency, department, or political subdivision from accepting or requiring payment in a CBDC or participating in any Federal Reserve pilot program involving such a currency.

The legislation also supports crypto mining activity. It restricts local governments from imposing specific sound limits on mining operations in industrial zones beyond general noise regulations and prevents targeted restrictions on mining businesses.

S. 163 also defines key blockchain-related terms, including digital assets, wallets, nodes, staking, and mining, providing legal clarity for developers and companies operating in the sector.

Several crypto-related activities are now exempt from money transmitter licensing requirements, including mining operations, node operation, crypto-to-crypto transactions, and development of onchain applications.

The move places South Carolina among a growing number of US states adopting crypto-friendly policies. Similar legislation was passed in Kentucky in 2025, which also protected self-custody rights and restricted local governments from targeting mining operations.

The new law signals a broader push among state governments to define digital asset rights independently from federal frameworks, particularly around custody, payments, and blockchain infrastructure development.

Disclaimer: All materials on this site are for informational purposes only. None of the material should be interpreted as investment advice. Please note that, despite the nature of much of the material created and hosted on this website, HODL FM operates as a media and informational platform, not a provider of financial advisory services. The opinions of authors and other contributors are their own and should not be taken as financial advice. If you require advice, HODL FM strongly recommends contacting a qualified industry professional.