South Korea launched its first crypto exchange in 2013. That exchange was Korbit. Most platforms from that era are long gone, but Korbit kept going through multiple market crashes, aggressive regulatory overhauls, and a complete reshaping of how Korean crypto operates. In 2026, it's still regulated, still active, and sitting on the edge of its biggest ownership change yet. This review covers what the Korbit crypto exchange actually offers right now, what you'll pay, and whether it's worth your time. It's based on verified data from CoinGecko, CoinMarketCap, and current regulatory records. The platform was not tested with live funds. For a broader look at the local market, see the top crypto exchanges in South Korea.

What is Korbit?

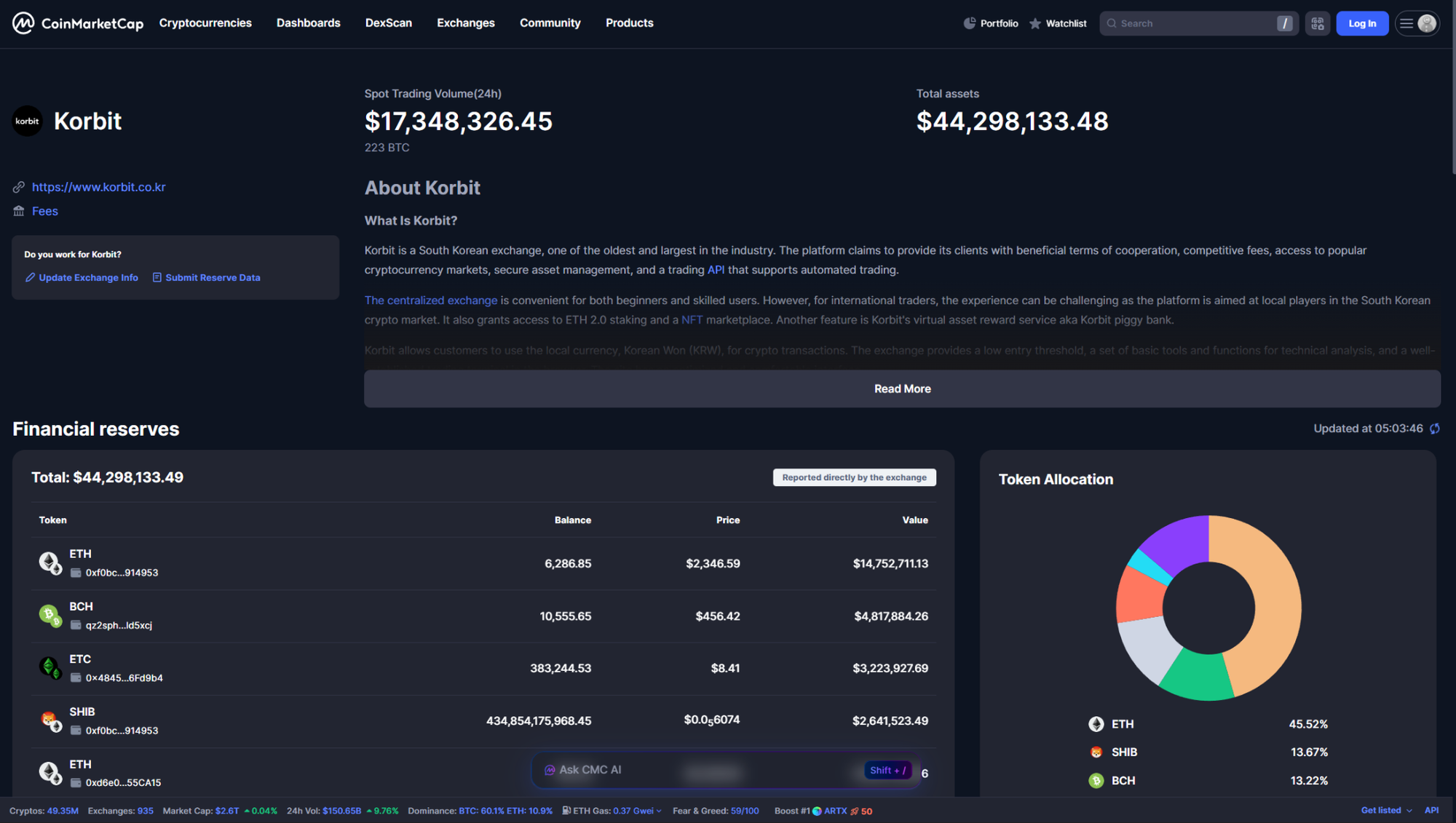

Korbit is a centralized crypto exchange built entirely around the Korean won. You link a verified Korean bank account, deposit KRW, buy crypto, and withdraw back to the same account. Everything on the platform runs through KRW pairs, which keeps the experience straightforward for local users but creates real barriers for anyone outside South Korea. According to Korbit's live stats on CoinGecko, the platform currently lists 182 coins and 183 trading pairs with around $52.8 million in reported 24-hour volume. It sits in South Korea's 'Big Four' alongside Upbit, Bithumb, and Coinone, all headquartered in Seoul.

One big change is happening. Mirae Asset Financial Group, an investment firm in Korea, is trying to buy Korbit. If it happens, Mirae Asset will be the first big Korean financial institution to have a crypto exchange. This deal was still not done in April 2026.

Features of Korbit

Korbit keeps things focused. It covers the tools most retail traders actually need and adds a few useful extras beyond basic spot trading.

Spot trading

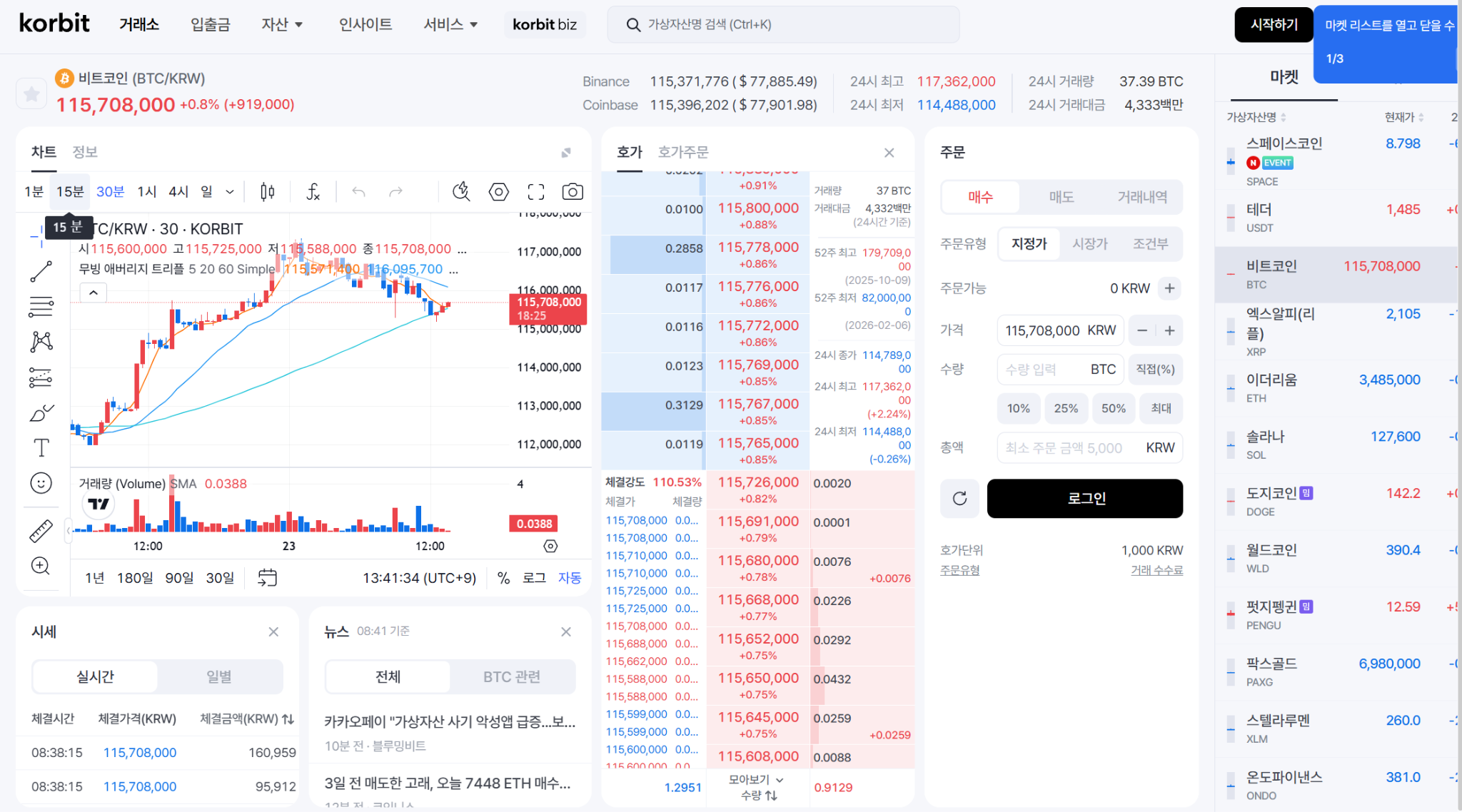

You can trade BTC, ETH, XRP, SOL, ADA, DOGE, USDC, and many more assets, all paired with Korean won. No leverage, no futures, no derivatives. Built for investors who want to own actual coins rather than trade contracts.

Staking, lending, and bots

Korbit allows users to stake ETH 2.0, use the Piggy Bank service for earning passive income, and trade on the NFT exchange, according to details provided by CoinMarketCap. Korbit's coin lending enables borrowers to obtain cryptocurrency loans by using various digital coins and KRW as collateral with 12 options, such as Bitcoin (BTC), Ethereum (ETH), Tether (USDT), and USDCoin (USDC).

Korbit app

The Korbit app is available on Android and iOS, covering trading, deposits, withdrawals, and staking. It's reasonably well-optimized for a mobile experience. The English version is still listed as coming soon, so non-Korean speakers will need a translation tool to navigate it comfortably.

Is Korbit safe?

This is genuinely Korbit's strongest selling point. To legally accept KRW deposits in South Korea, an exchange must complete VASP registration with the Financial Intelligence Unit and hold a real-name bank account agreement with a domestic bank. Only five exchanges qualified as of early 2026, and Korbit is one of them, partnered with Shinhan Bank.

Korbit keeps 80% of assets in cold storage, uses AES-256 encryption, and requires 2FA for logins, deposits, and withdrawals. The FIU did fine Korbit around $2 million for AML failures. They paid it, didn't appeal, and committed to better monitoring. No hacks on record since 2013, though there's no deposit insurance on crypto assets.

Trading experience and Korbit fees

The system is based on the TradingView Terminal, which operates in the web browser, offering the ability to use both limit and market orders. The design is quite nice and easy to understand for newbies, yet still appealing to professional traders. But the feature that is not available here is leverage.

Concerning the fees, Korbit's trading fee rates, based on volume, begin with a maker fee of 0.08% and a taker fee of 0.20%. Traders that generate more than 100 billion KRW in their monthly volume will get zero maker fee, while the taker fee goes down to 0.01%. Deposits are free for both KRW and crypto. KRW withdrawals have a flat 1,000 KRW fee per transaction. Crypto withdrawal fees vary by coin, and Bitcoin costs 0.00001 BTC per transaction.

Pros and cons of Korbit

Here's a quick summary of where Korbit stands.

Korbit alternatives

According to Tiger Research's 2026 Korea crypto market guide, Upbit and Bithumb together hold around 87% of the domestic market, Coinone sits at roughly 10%, and Korbit holds under 1%. That gap shows up directly in order book depth and liquidity.

Upbit holds the top position among the exchanges with high liquidity and volumes, collaborating with K-Bank. Bithumb ranks as the second-biggest exchange, working with KB Kookmin Bank. It has higher liquidity than Korbit. Coinone works with Kakao Bank, making it widely accessible through the Kakao app suite.

Is Korbit worth using?

In terms of a regulated platform that allows for an easy entry point for people from Korea into the crypto industry, Korbit would make a decent pick. Notably, their commissions are relatively favorable, they have had no issues with their security, and, most importantly, it is possible to stake and lend one's coins with Korbit, adding additional value to the trading process.

In the case of Mirae Asset acquiring the asset, the services offered by the platform will be upgraded significantly. If the deal goes through, Mirae Asset has signaled plans to tokenize real-world assets like property and bonds, with Korbit handling distribution. Korbit hasn't confirmed the specifics yet, so treat it as a likely direction rather than a guarantee.

Nevertheless, the platform still remains limited due to several factors. Namely, it has less trading activity than Upbit and Bithumb, provides no leverage opportunities for active traders, customer service is only available in Korean, and strict regulations concerning banks make it unavailable to foreign users. Still, Korbit can be considered a well-regulated exchange with positive past performance records and steady improvements.

Disclaimer: All materials on this site are for informational purposes only. None of the material should be interpreted as investment advice. Please note that, despite the nature of much of the material created and hosted on this website, HODL FM operates as a media and informational platform, not a provider of financial advisory services. The opinions of authors and other contributors are their own and should not be taken as financial advice. If you require advice, HODL FM strongly recommends contacting a qualified industry professional.