Most individuals come across Aave in a similar fashion. You get some information about it from some crypto community, do some research online and realize you have no idea what liquidity pools are, and you question yourself about using any platform which is not insured by any bank. This review will go through how Aave protocol operates, its fees, risk management, and other vital information.

What is Aave?

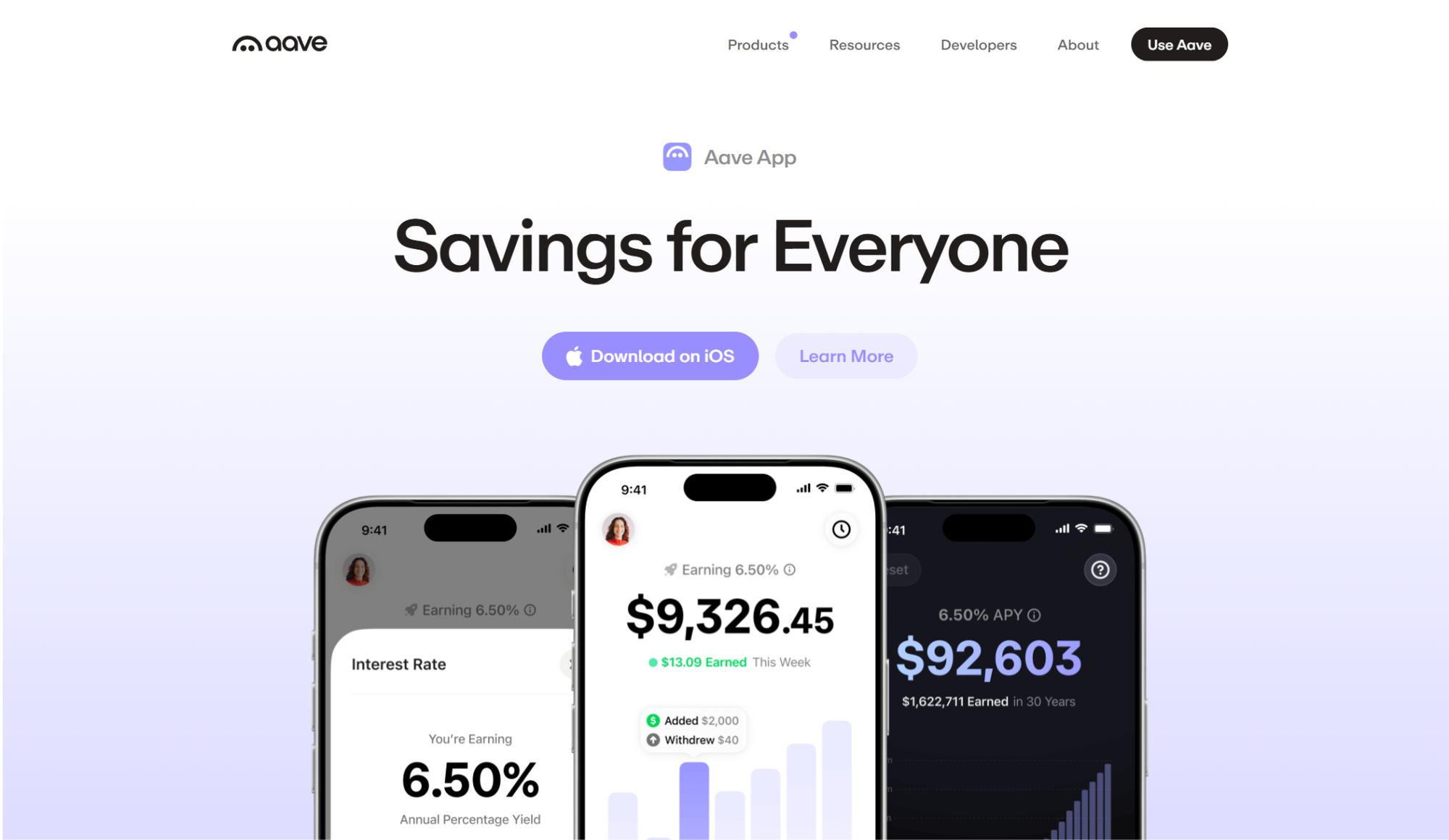

Aave is a decentralized lending platform. You can deposit crypto to earn interest, or borrow crypto by putting up your own crypto as collateral. You don't need a bank account, a credit check, or any ID. Everything runs on smart contracts, code that handles the logic automatically on the blockchain.

Aave was formerly known as ETHLend, which transformed its structure to incorporate shared liquidity pools and rebranded itself as Aave in 2020. It currently operates on V3, but the approval for V4 is underway. According to an April 2026 report by Spoted Crypto, Aave became the first decentralized finance (DeFi) protocol to surpass $1 trillion in total lending volume in February 2026.

Features of Aave

A few things make Aave stand out from other crypto lending platforms.

Flash loans

Borrow large amounts with zero collateral, as long as everything is repaid in a single transaction. According to Aave, it charges just 0.05% per flash loan on V3. Mostly used by developers and arbitrage traders.

aTokens

Deposit crypto and you get aTokens back. They grow in value automatically as interest accrues. Deposit USDC, get aUSDC, watch it appreciate over time. You can also use aTokens elsewhere in DeFi while they're still earning.

GHO stablecoin and multi-chain

Aave has its own stablecoin called GHO, with supply now past $580 million according to CoinMarketCap data. The protocol also runs across 20+ chains, including Arbitrum, Polygon, Avalanche, and Base, which gives real flexibility on gas costs.

Is Aave safe and legit?

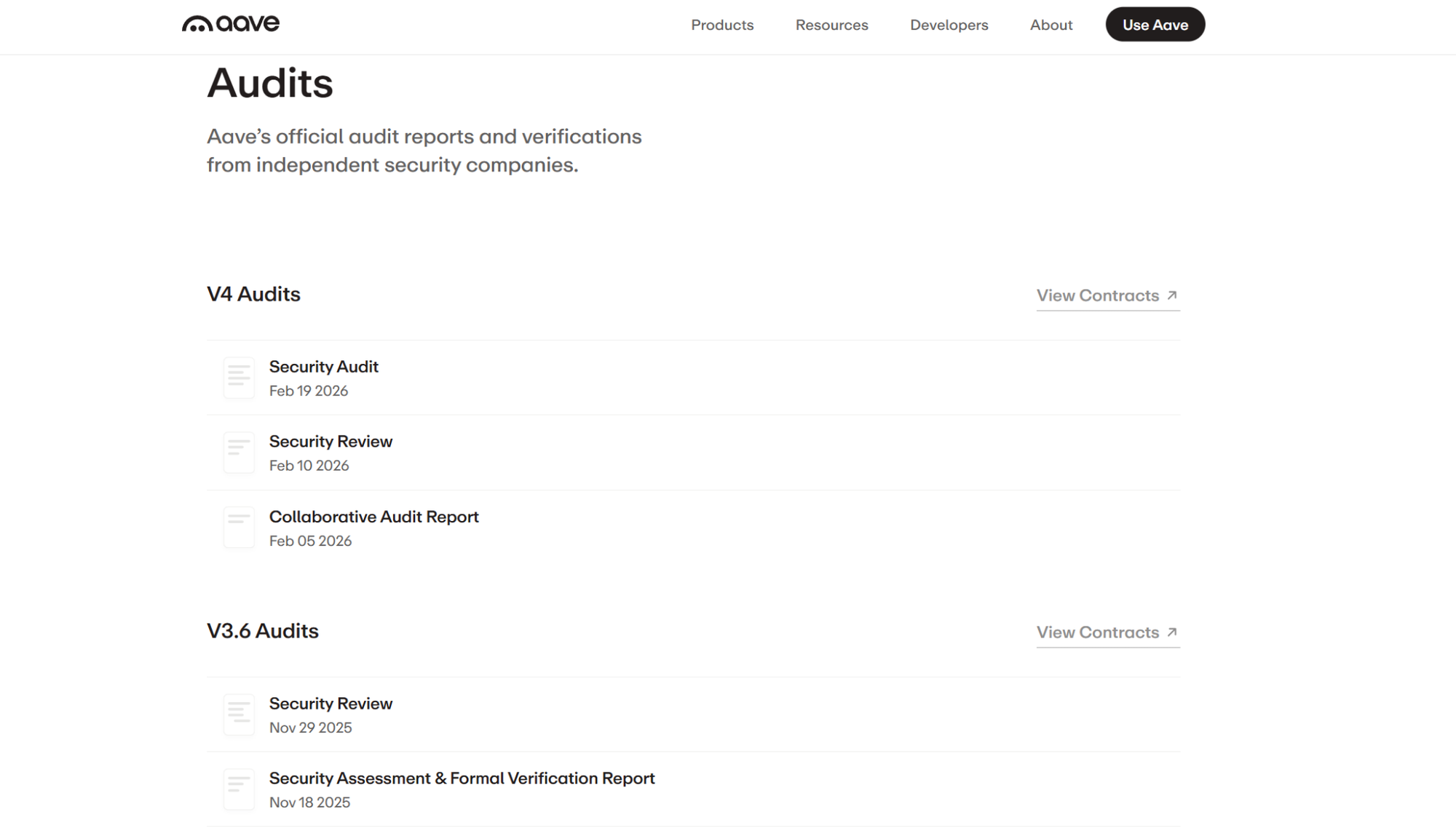

Aave's track record is genuinely solid. According to Aave's security page, the protocol holds over $246 million in safety reserves. For V4, The Block reported in March 2026 a $1.5 million audit program involving ChainSecurity, Trail of Bits, and Blackthorn, plus a public security contest where 900+ researchers submitted 950+ findings with no critical vulnerabilities found.

April 2026 put their reputation to the test. Hackers managed to take advantage of the bridge used by KelpDAO and extract around $292 million worth of rsETH tokens, using them as collateral to borrow against via Aave V3. As per CoinDesk, none of the smart contracts at Aave were affected, but $196 million worth of bad debts came into existence.

The situation got messier from there. As reported by HodlFM, Mantle had an active Aave loan backed by rsETH at the time of the exploit. When rsETH's value collapsed, that position came under serious pressure and added to the bad debt problem already unfolding across the protocol. It's a good example of how one hack can create a chain reaction across DeFi. Aave quickly shut down impacted markets. The smart contract worked, but external threats in DeFi are present.

User experience and interface

After connecting a wallet and testing deposits on Arbitrum, the setup took under five minutes. The interface on Aave is cleaner than many other DeFi services, though it's not ready for immediate use. One needs to first link their Web3 wallet (e.g., Metamask). With that done, a dashboard displays deposits, borrows, and a real-time health factor indicating distance from liquidation.

Repayments can be made with the borrowed asset or with collateral, in full or in part, with no fixed schedule. Better for people who already know DeFi basics.

Fees and Aave interest rates

There is no sign-up fee or platform subscription. Your cost is determined by your usage.

Borrowing rates

Rates are variable. USDC borrowing typically runs 2% to 8% in normal conditions and can spike above 15% during high-demand periods. Aave's app shows up to 6.50% APY for lenders on stablecoins.

Gas and liquidation

The gas depends on the network you will employ. Arbitrum and Base chains are significantly cheaper than the Ethereum mainnet. As per liquidations in the case of Aave, based on their documentation, if your health factor is less than 1, then liquidators can pay off up to 50 percent of your debt, along with a 5 percent bonus from your ETH.

Pros and cons of Aave

Here's a quick side-by-side.

Aave alternatives

Aave isn't the only DeFi lending option. Here's how it stacks up, using current data from DefiLlama.

Is Aave worth using in 2026?

For people who know DeFi, yes. According to Spoted Crypto, Aave generated over $83 million in protocol fees in a single 30-day window. V4 is rolling out, institutional adoption through Aave Horizon is growing, and the core code has never been broken.

For beginners, however, it's a bit more complex. The Defi system places all of the risk management on you. According to Blockchain Magazine's April 2026 analysis, Aave maintained LTV ratios between 70%-82%, whereas other competitors were moving towards ratios between 85%-90%.

Final thoughts

Aave is the most tested lending protocol in DeFi. The code hasn't been directly exploited. It crossed $1 trillion in all-time loans earlier this year and runs one of the most thorough audit programs in the space.

Just don't mistake solid for risk-free. Understand your health factor, know your liquidation threshold, and don't deposit more than you're comfortable managing actively. Done right, Aave is one of the better tools decentralized finance has right now.

Disclaimer: All materials on this site are for informational purposes only. None of the material should be interpreted as investment advice. Please note that, despite the nature of much of the material created and hosted on this website, HODL FM operates as a media and informational platform, not a provider of financial advisory services. The opinions of authors and other contributors are their own and should not be taken as financial advice. If you require advice, HODL FM strongly recommends contacting a qualified industry professional.