The U.S. Department of Labor has introduced a proposed rule that could reshape how retirement savings are invested in the United States. The draft, released by the department’s Employee Benefits Security Administration, would allow 401(k) plan fiduciaries to consider a broader range of assets, including cryptocurrencies, private equity, and real estate, under a clearer regulatory framework.

The proposal follows an executive order from Donald Trump that directed federal agencies to expand access to non-traditional investments in retirement accounts. Officials describe the move as part of a wider effort to align retirement investing with modern financial markets.

A shift toward process-based oversight

At the center of the proposal is a reaffirmation of fiduciary duties under the Employee Retirement Income Security Act. The rule emphasizes that fiduciary responsibility depends on a prudent and well-documented decision-making process rather than the outcome of specific investments.

Plan managers would retain discretion to include alternative assets if they evaluate key factors such as fees, liquidity, valuation, performance benchmarks, and overall complexity. The draft introduces a “safe harbor” framework that aims to reduce litigation risk for fiduciaries who follow these steps.

“This greater diversity will drive innovation and result in a major win for American workers, retirees, and their families,” said Labor Secretary Lori Chavez-DeRemer.

Deputy Labor Secretary Keith Sonderling reinforced the department’s neutral stance. “The department's days of picking winners and losers are over,” he said, pointing out that fiduciaries must apply consistent evaluation standards across all asset classes.

Crypto returns to the table

The proposal could reopen the door for digital assets such as Bitcoin within retirement plans. While fiduciaries have never been explicitly barred from offering crypto exposure, earlier federal guidance discouraged such moves.

In 2022, the Biden administration urged plan sponsors to exercise “extreme care” before including cryptocurrencies, citing volatility and investor protection concerns. That guidance had a chilling effect, according to the Labor Department, with very few plans offering alternative investments.

The new rule does not endorse any specific asset class. Instead, it defines digital assets as a category that includes cryptocurrencies and other token-based investments. It places them on equal regulatory footing with other alternatives, provided fiduciaries conduct proper due diligence.

Treasury Secretary Scott Bessent said the proposal represents an initial step toward implementing the administration’s directive.

“This proposed rule is an initial step in implementing the President's Executive Order in a safe and smart manner, broadening access to additional retirement plan options for millions of Americans while being mindful of the importance of protecting retirement assets,” he said.

Trillions in retirement assets at stake

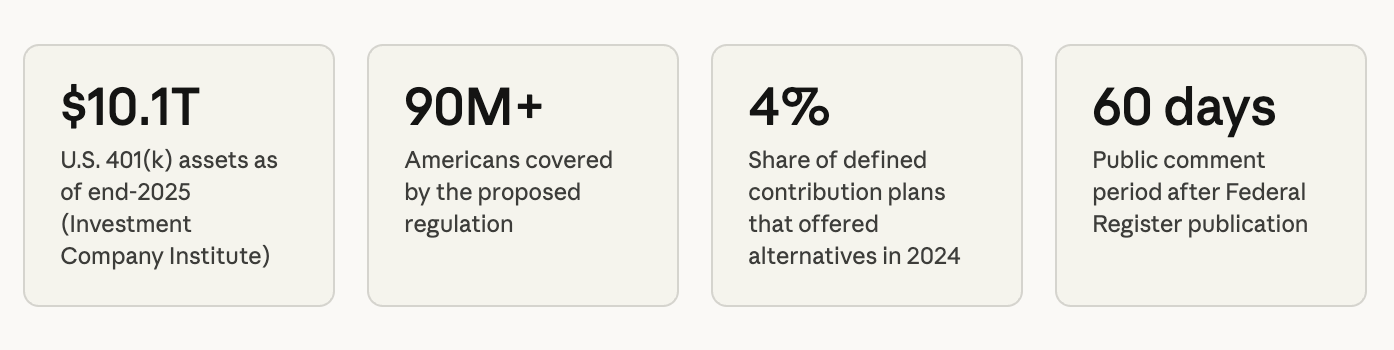

The scale of the U.S. retirement market underscores the potential impact of the rule. Americans held approximately $10.1 trillion in 401(k) plans at the end of 2025, according to data from the Investment Company Institute. Despite that size, only a small fraction of plans currently include alternative assets.

The Labor Department noted that roughly 4% of defined contribution plans offered such investments last year, with only 0.1% of total assets allocated to them. The proposal seeks to address this gap by clarifying the legal framework and reducing perceived liability risks.

Regulators from the U.S. Securities and Exchange Commission and the U.S. Department of the Treasury contributed to the rulemaking process. Their involvement signals a coordinated approach to modernizing retirement investment policy.

Industry positioning and allocation strategies

Large asset managers have already outlined potential allocation strategies in anticipation of regulatory clarity. Morgan Stanley has suggested a 2% to 4% allocation to digital assets in diversified portfolios, while BlackRock has recommended a more conservative range of 1% to 2%.

The proposal could also accelerate the development of new financial products tailored for retirement accounts, including managed crypto funds and exchange-traded structures designed to meet liquidity and pricing requirements.

Political pushback and risk concerns

Not all policymakers support the initiative. Senator Elizabeth Warren criticized the proposal, warning that it could expose retirement savings to unnecessary risk.

As cracks emerge in private credit, private equity returns fall to 16-year lows, and crypto keeps tumbling, Trump has decided now is the time to stick these risky assets into Americans’ 401(k)s.

— Elizabeth Warren (@SenWarren) March 30, 2026

Another day, another Trump policy putting Wall Street first – and workers last.

The debate highlights a longstanding tension within retirement investing. Long-term horizons can support exposure to emerging technologies, but strict risk controls and regulatory obligations often limit adoption.

What comes next

The proposal has been published in the Federal Register under the title “Fiduciary Duties In Selecting Designated Investment Alternatives” and is now open for a 60-day public comment period. During this time, industry participants, policymakers, and the public can provide feedback before any final rule is adopted.

If finalized, the regulation could mark a structural shift in how Americans build retirement portfolios. Even modest allocations to alternative assets could introduce significant new capital flows into markets such as crypto.

For now, fiduciaries face a familiar challenge. They must balance innovation with risk management while navigating a clearer, but still evolving, regulatory landscape.

Disclaimer: All materials on this site are for informational purposes only. None of the material should be interpreted as investment advice. Please note that, despite the nature of much of the material created and hosted on this website, HODL FM operates as a media and informational platform, not a provider of financial advisory services. The opinions of authors and other contributors are their own and should not be taken as financial advice. If you require advice, HODL FM strongly recommends contacting a qualified industry professional.