Blockchain analytics firm Chainalysis projects that stablecoin transaction volumes could reach $1.5 quadrillion annually by 2035, potentially exceeding the combined off-chain volumes of Visa and Mastercard. The firm released its findings in a preview of its forthcoming report, “The New Rails: How Digital Assets Are Reshaping the Foundations of Finance.”

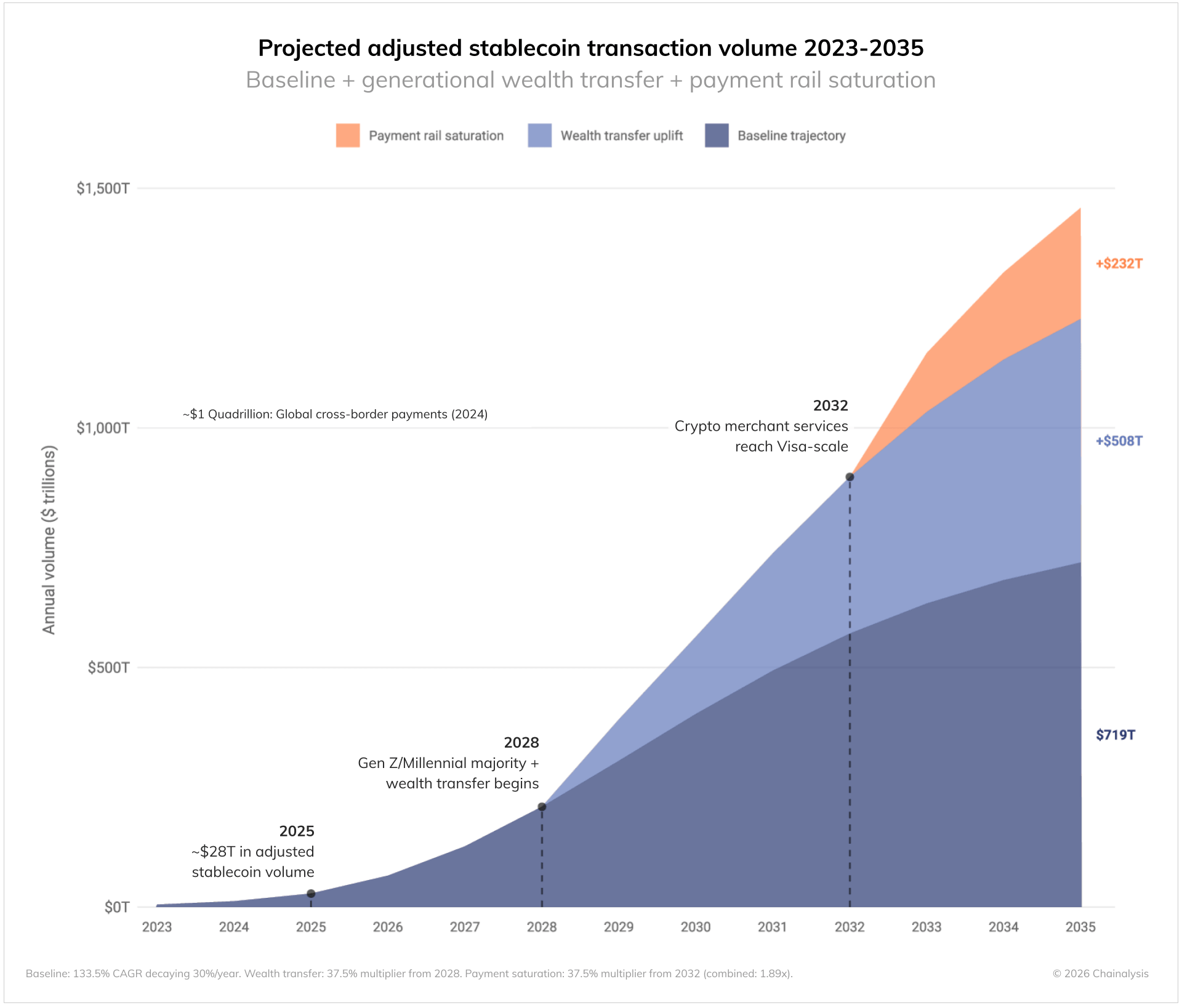

According to Chainalysis, adjusted stablecoin volume, which filters out non-economic activity such as wash trading or bot-driven transfers, grew at a 133% compound annual growth rate between 2023 and 2025, reaching $28 trillion in real economic activity. The firm estimates that organic growth alone could push volumes to $719 trillion by 2035.

Generational wealth transfer drives adoption

Two macro trends underpin this projection. The first is the transfer of wealth from Baby Boomers to Millennials and Gen Z. Between 2028 and 2048, an estimated $100 trillion will move to younger generations who are more likely to adopt crypto as a default financial tool. Nearly half of Millennials and Gen Z have held or currently hold crypto, according to a 2025 Gemini survey.

Chainalysis estimates that this demographic shift alone could add $508 trillion to annual stablecoin volumes by 2035.

Point-of-sale integration expands usage

The second trend is stablecoin adoption at the point of sale. As merchants integrate stablecoins into their payment systems, paying with crypto transitions from a deliberate choice to standard infrastructure, similar to how credit cards overtook cash. Chainalysis projects that point-of-sale adoption could contribute another $232 trillion to annual volumes by 2035.

The firm noted that current growth trajectories place stablecoin payments on pace to match Visa and Mastercard’s off-chain transaction volumes sometime between 2031 and 2039.

Institutional activity signals market shift

Traditional financial companies are already positioning for widespread stablecoin adoption. Stripe acquired Bridge for $1.1 billion, while Mastercard formed a partnership with BVNK in a deal valued at up to $1.8 billion.

“These are operational bets, not experiments. Add regulatory clarity from the GENIUS Act, and institutional participation can scale in ways that simply were not possible before,” Rachael Lucas, a crypto analyst at BTC Markets, told Cointelegraph.

The GENIUS Act, signed into law by former President Donald Trump, signaled serious regulatory momentum in the U.S., making stablecoins a core consideration for financial services firms.

Crypto-native generations reshape finance

The ongoing wealth transfer, combined with point-of-sale saturation, represents a fundamental shift in how financial products function. Millennials and Gen Z are the first generations for whom on-chain transactions are a default, not a deliberate choice. Surveys indicate growing crypto activity among these groups: a January OKX survey reported that 40% of Gen Z and 36% of Millennials plan to increase crypto usage in 2026, compared with 11% of Boomers.

“This shift could reshape the competitive landscape for payments in ways that traditional institutions can no longer ignore,” Chainalysis noted.

Stablecoins as programmable and global rails

Unlike legacy payment systems, stablecoins settle in seconds, operate 24/7, and bypass correspondent banking layers. These features reduce transaction costs, accelerate finality, and enable programmable money. Businesses already use stablecoins for remittances, B2B payments, and treasury operations, and adoption is poised to grow further as infrastructure and regulatory clarity improve.

With adjusted volumes potentially surpassing $1 quadrillion, stablecoins could redefine global payments within the next decade. Institutions that fail to integrate on-chain rails may risk losing capital and market share to new, crypto-native infrastructure.

Disclaimer: All materials on this site are for informational purposes only. None of the material should be interpreted as investment advice. Please note that, despite the nature of much of the material created and hosted on this website, HODL FM operates as a media and informational platform, not a provider of financial advisory services. The opinions of authors and other contributors are their own and should not be taken as financial advice. If you require advice, HODL FM strongly recommends contacting a qualified industry professional.